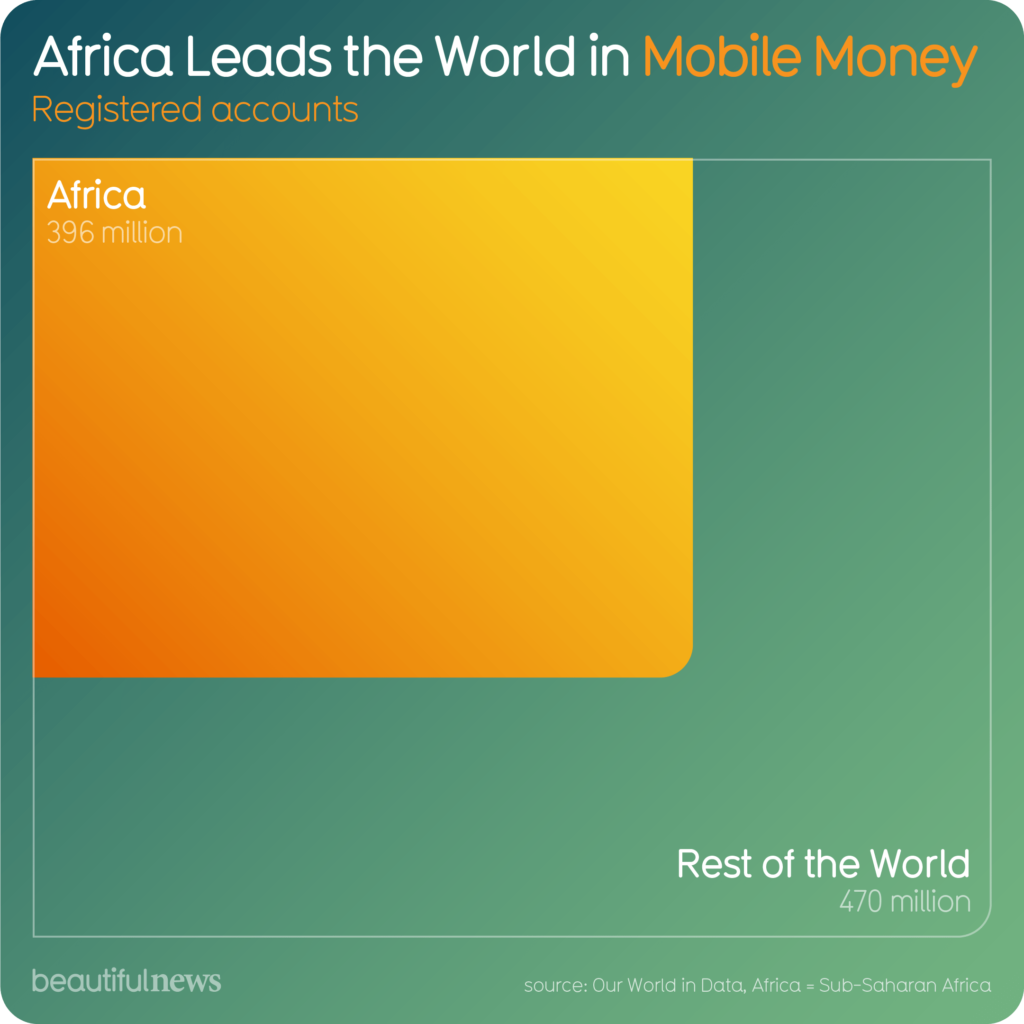

For years, Africa has dazzled the world with its mobile money revolution. This phenomenon, often hailed as a “leapfrog” moment, has seen the continent become a global leader in mobile money accounts. Sub-Saharan Africa alone boasts 396 million registered accounts, rivalling the rest of the world’s 470 million. It is a success story celebrated by development economists and tech evangelists alike, often framed as a triumph of innovation over infrastructure limitations. Yet, behind the applause lies a more nuanced truth: while Africa leads in mobile money, the rest of the world is charging ahead in the broader race for real digital financial transformation.

Mobile money is undoubtedly a milestone, providing millions with access to basic financial services. But as we celebrate Africa’s mobile money achievements, a critical question arises: does this success translate to true financial innovation? The answer lies in examining the broader global landscape.

In Europe, the Americas, and parts of Asia, the conversation has shifted beyond simple financial inclusion to transformative technologies that integrate seamlessly into daily life. Blockchain is revolutionising payments, lending, and even identity verification. Digital banks are offering full-service, mobile-first platforms that rival traditional institutions. Integrated payment systems are enabling frictionless transactions that work across borders, currencies, and platforms. These developments are not just evolutionary steps; they are building the financial infrastructure of the future.

In contrast, Africa’s mobile money systems—dominated by telecom-led platforms like M-Pesa—are still largely confined to basic services such as peer-to-peer transfers, bill payments, and airtime purchases. They solve immediate challenges but fall short of the sophisticated capabilities now defining global financial systems.

Take blockchain as an example. In the United States, blockchain technology is being leveraged to reimagine global payments, remittances, and asset ownership. Companies like Ripple and Ethereum-based platforms are providing faster, cheaper alternatives to traditional bank wires and cross-border transfers.

Meanwhile, central banks in Europe and China are experimenting with Central Bank Digital Currencies (CBDCs), which could redefine monetary policy and financial regulation. The European Union, through its Digital Euro initiative, is pioneering efforts to digitise currency while safeguarding data privacy and security.

In Africa, blockchain remains largely underexplored. While countries like Nigeria and South Africa have flirted with blockchain for cryptocurrencies and tokenisation, large-scale adoption is hampered by regulatory uncertainty, infrastructure challenges, and lack of investment. The technology is often viewed with suspicion, linked more to speculative crypto trading than as a foundational tool for financial transformation.

Digital banks are another area where the rest of the world is racing ahead. Neobanks like Monzo, Revolut, and Nubank are redefining banking with their sleek, mobile-first interfaces and hyper-personalised services. These platforms are more than glorified apps; they offer savings accounts, investment tools, and financial analytics, all backed by robust digital ecosystems.

Latin America’s Nubank, for example, has amassed over 85 million customers by offering seamless, low-cost financial services tailored to its users’ needs. Asia’s digital banks, such as WeBank in China and KakaoBank in South Korea, have integrated artificial intelligence and big data analytics to create predictive financial products that anticipate customer behaviour.

Africa’s mobile money platforms pale in comparison. While they have expanded access to financial services, they operate in a relatively siloed fashion. Few provide the integrated, data-driven solutions that characterise digital banks elsewhere. Efforts to build similar ecosystems in Africa, such as Nigeria’s Flutterwave or South Africa’s TymeBank, are promising but remain in their infancy compared to their global counterparts.

The rise of integrated payment systems further underscores Africa’s lag. In countries like Sweden, cash is practically obsolete, replaced by platforms like Swish that combine banking, retail, and peer-to-peer payments into one seamless ecosystem. China’s Alipay and WeChat Pay go even further, embedding financial transactions into social and commercial platforms. Users can book a taxi, pay for groceries, and invest in mutual funds—all within a single app.

In contrast, Africa’s mobile money platforms are still grappling with interoperability. Despite initiatives to enable cross-network transactions, many systems remain fragmented, forcing users to navigate a patchwork of services. Cross-border payments, a lifeline for the continent’s diasporas, remain costly and cumbersome, despite the promise of mobile money to simplify these transactions.

Africa’s mobile money success is often framed as a leapfrog story, where the continent has bypassed traditional banking infrastructure to embrace digital solutions. But the leapfrog narrative risks becoming a trap if it leads to complacency. Mobile money addresses immediate needs, but without investment in advanced technologies like blockchain, artificial intelligence, and integrated systems, Africa risks being left behind in the next wave of financial innovation.

Governments and private sectors across the continent must reimagine what financial inclusion means. It is no longer enough to provide access; the goal must be to build financial systems that empower users to save, invest, and participate in the global economy on equal footing. This requires robust digital infrastructure, clear regulatory frameworks, and a willingness to experiment with emerging technologies.

Africa’s mobile money story is an inspiration, but it is not the end of the journey. The rest of the world is not waiting, and neither should Africa. The future of finance lies in systems that are not only inclusive but also integrated, innovative, and globally competitive.

The time has come for Africa to move beyond the basics and invest in the financial technologies that will define the next decade. Only then can it truly lead—not just in mobile money accounts, but in the broader, more meaningful race for digital financial transformation.

vkdlkurmmruvjiqquoeonljtsgzogq